Tips for buying a new car from a dealership

Doing homework on vehicles, loan rates and car prices might help keep the process from being overwhelming.

Want tips for buying a new car or new-to-you used car? Either can seem overwhelming. Not only do you have to choose among dozens of vehicle options, but you also have to arrange financing and possibly get rid of your current car. Additionally, you usually need to prove that you have insurance before you can drive off the lot, but it's relatively easy to obtain proof of insurance and to add or replace a vehicle on your existing insurance policy. Here are some car buying tips to help you buy in confidence.

What should I do before I buy a car, truck or SUV?

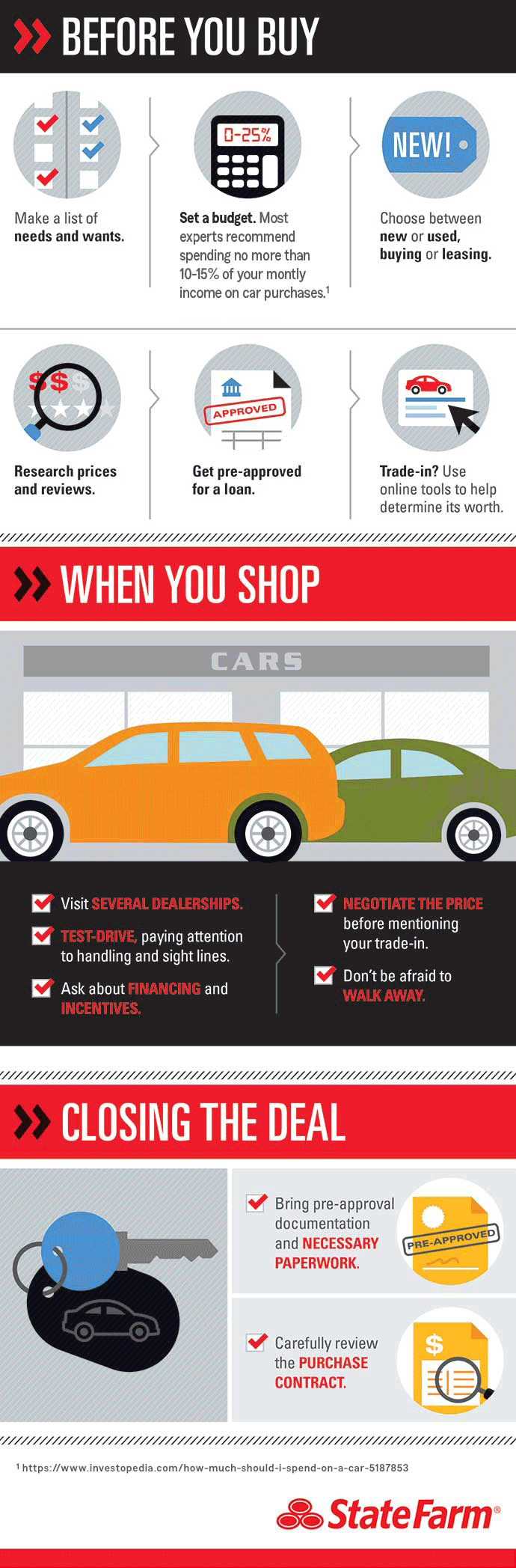

- Make a list of needs and wants. When it comes time to find the one, options are endless. Consider what matters to you and your daily driving needs. For example, stop-and-go traffic routes may equal an emphasis on mpg to save gas. If you constantly haul loads (or extra kids), you may need a roomier fit and a bigger vehicle. Do you want room for a family or additional cargo space? Do you want rear view cameras or other features that improve car safety? Are you looking for efficient gas mileage on highways or in town driving? Once you have your list, search on car finder sites to find models that meet your needs. Pick three models to research further.

- Find out how the insurance industry ranks your vehicle. A "new-to-you" car may equal a new-to-you insurance rate. The total will depend on the car's make, model, policy specifics and other information. See how your desired cars rank in insurance cost as compared to other cars. Also, check with your insurance agent to get an estimate of how much insurance will be on your new vehicle.

- Set a budget. Most experts recommend spending no more than 10-15% of your monthly income on vehicle purchases. Use online calculators to understand whether your cars' monthly payments fit within your budget.

- Choose between new or used, buying or leasing. Owning establishes equity, which means when you sell the vehicle you'll reap any difference between the loan you have left and the value you own in the car. But owning means you're responsible for everything, including pricey repairs. Leasing equals no equity but often lower monthly payments and less money down. However, if you're constantly driving long distances, there are lease mileage restrictions. Use an online calculator to help determine if you should lease or buy your next vehicle.

- Research prices and reviews. Manufacturers' websites have a wealth of information about the costs of certain features, colors and trim levels. Various research companies like Consumer Reports, Carfax, J.D. Power and Kelly Blue Book collect maintenance reports from a variety of sources on vehicles. Kelley Blue Book has a Five-Year Cost to Own breakdown and Consumer Reports has a Cost of Vehicle Ownership article that can show you the true cost of ownership for any vehicle.

- Get pre-approved for a loan. Whether you choose to buy or lease, your credit history matters. Work with your financial institution ahead of time to secure an auto loan and an interest rate. A car loan pre approval may be used as a bargaining tool when you negotiate with the dealership.

- Know your credit score. Check beforehand so you're confident about what you can afford, and triple-check all numbers in your paperwork.

- Utilize online tools. Free car appraisal tools on the internet can approximate how much your car may be worth. Check multiple sites and be realistic when evaluating the condition of your vehicle. Very few cars actually qualify as "excellent." And be honest when discussing your trade-in with the dealer — a service evaluation can quickly discover any service needs.

- Shop around your trade-in. Just because an appraisal tool indicates your car is worth $5,000 doesn't mean you'll get that amount from a dealer. They may have a surplus of that make and model, and may also have promotions or profit goals that affect any trade-in offers. Tip: To get an idea of the range of offers, visit several dealers, including at least one that is different from your car's brand.

What should I consider when shopping at a dealership?

- Visit several dealerships. Dealerships have different inventories. Checking multiple dealerships might help ensure you will get the features, colors and price you are looking for. Most dealerships publish their inventories online, making finding the right vehicle even easier. Sites such as Autotrader.com or CarGuru.com can help you search beyond your local dealership.

- Test-drive vehicles. Navigating cars on paper and on websites is one thing, but driving is essential. Set aside at least 30 minutes to test drive your top choice (include city and freeway routes), and then drive several other vehicles. Sit in the car while it's parked so you can review the interior. Pay attention to how a vehicle handles and its sight lines. Select a route to drive that includes hills, rough pavements, curves and even a stretch of highway.

- Ask about rebates and incentives. Most manufactures discount the cost of cars through rebates, or offer incentives to dealerships to sell the car. They usually change monthly and are listed on manufacturer websites. These incentives and rebates might help lower the cost of the vehicle.

- Negotiate price before mentioning your trade-in. If you can't get a dealer to budge on the price of a new car, you might be able to ask them to improve the total value of your trade-in as a lure for getting your business.

- Don't be afraid to walk away. One way to avoid the hard sell is by negotiating with dealerships via email after you've completed the test drive. Contact the sales manager about the model you want and the price you're willing to pay. If you're working with someone in person, know what you want, what you need and what you're willing to pay. Don't sign up for services or purchase a car that's beyond your budget.

- Don't negotiate based on your desired monthly payment. Often time, this results in higher down payments or increased loan lengths.

What should I pay attention to in the contracts?

- Bring pre-approval documentation and necessary paperwork. This might help streamline the process.

- Carefully review the purchase contract. Take your time and ask questions. Don't feel pressured into signing until you are ready.

- Make sure your trade-in is treated as credit. Once you agree on a value for the trade-in, make sure it's treated as a credit. This can help reduce the sales tax you pay on your new car purchase.

- Write down your interest rate. Never sign a deal or drive away in your new car if you don't see your interest rate in writing.

- Understand the sales tax and fees. Sales tax is a percentage of the cost of the car. Documentation fees are the cost the dealership charges for filling out the contract. Registration fees are paid to the state on behalf of the buyer.

What are some car dealership tricks to avoid?

According to DMV.org, here are a few dealership tactics to be cautious of when you're negotiating a new car price.

- Trade-in scams. Before signing any contracts, make sure the trade in value previously agreed upon is reflected in the final documents. Also, beware of "push, pull, tow sales." With these promotions, the trade-in value of your car actually comes from the rebates and incentives on the car you are purchasing. The rebates and incentives can be used to purchase the car regardless of the vehicle you are bringing in.

- Mixed negotiations. Also known as the "four-square" method, this salesman's trick combines multiple, unrelated factors into a single transaction. The sales manager writes the price of the car, the down payment, trade-in value and the desired monthly payment into four boxes. The numbers might not even relate to each other. If you are looking for a certain trade-in price or a set monthly payment, ensure the numbers being presented are used in the calculation.

- Inflated interest rates. Some car dealerships may advertise a certain interest rate, then they make last-minute changes to financing.

- Spot delivery. Some car buyers have driven a car off the lot without secured financing. This means that a few weeks later, the car dealership might call to say the loan application was rejected and they need new paperwork. If this happens, you could end up paying a higher interest rate or down payment.

- Poor credit. The dealership might play up the fact you have a low credit score, making you feel as if it's bad. Then they talk you into a higher down payment and possibly higher monthly payments.

- Negative equity. The dealership might tell you they are paying off your old loan when your car is not worth the remaining value of the loan. In reality, they are adding the "negative equity" on to the loan for your new car, or they're using the rebates and incentives to pay off the old loan.

- Avoid add on services like extra warranties or paint protection plans. Gap insurance is often suggested and can be overpriced. Shop around for these extra services if you are interested in them.

Whether you're buying a new car or purchasing a new-to-you used car, call your agent to discuss auto policy changes.